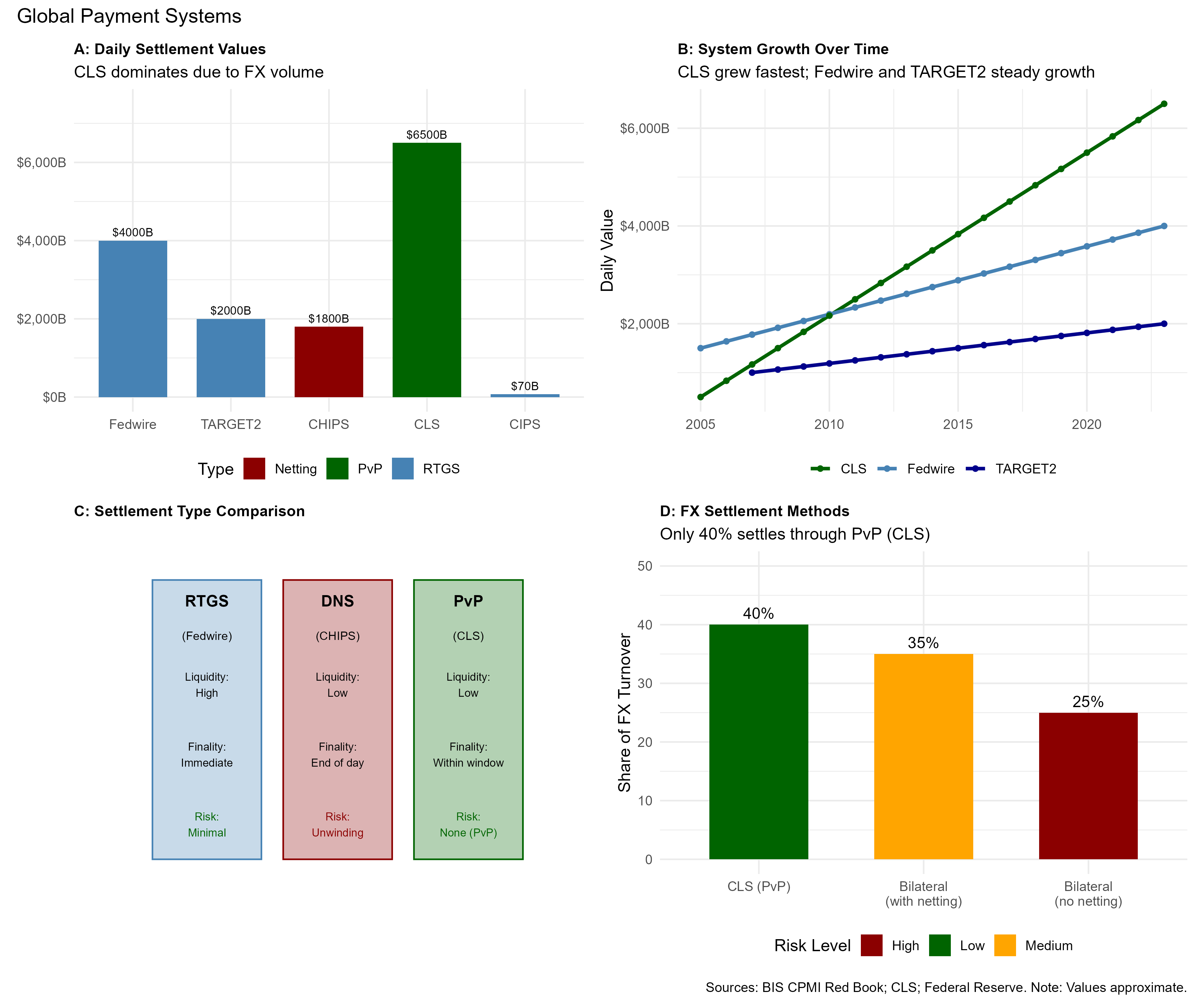

Figure 5.1: Payment System Volumes and Infrastructure. Large-value payment systems process trillions daily, forming the backbone of global finance. Source: BIS Red Book, Federal Reserve, ECB.

Figure 5.1: Payment System Volumes and Infrastructure. Large-value payment systems process trillions daily, forming the backbone of global finance. Source: BIS Red Book, Federal Reserve, ECB.

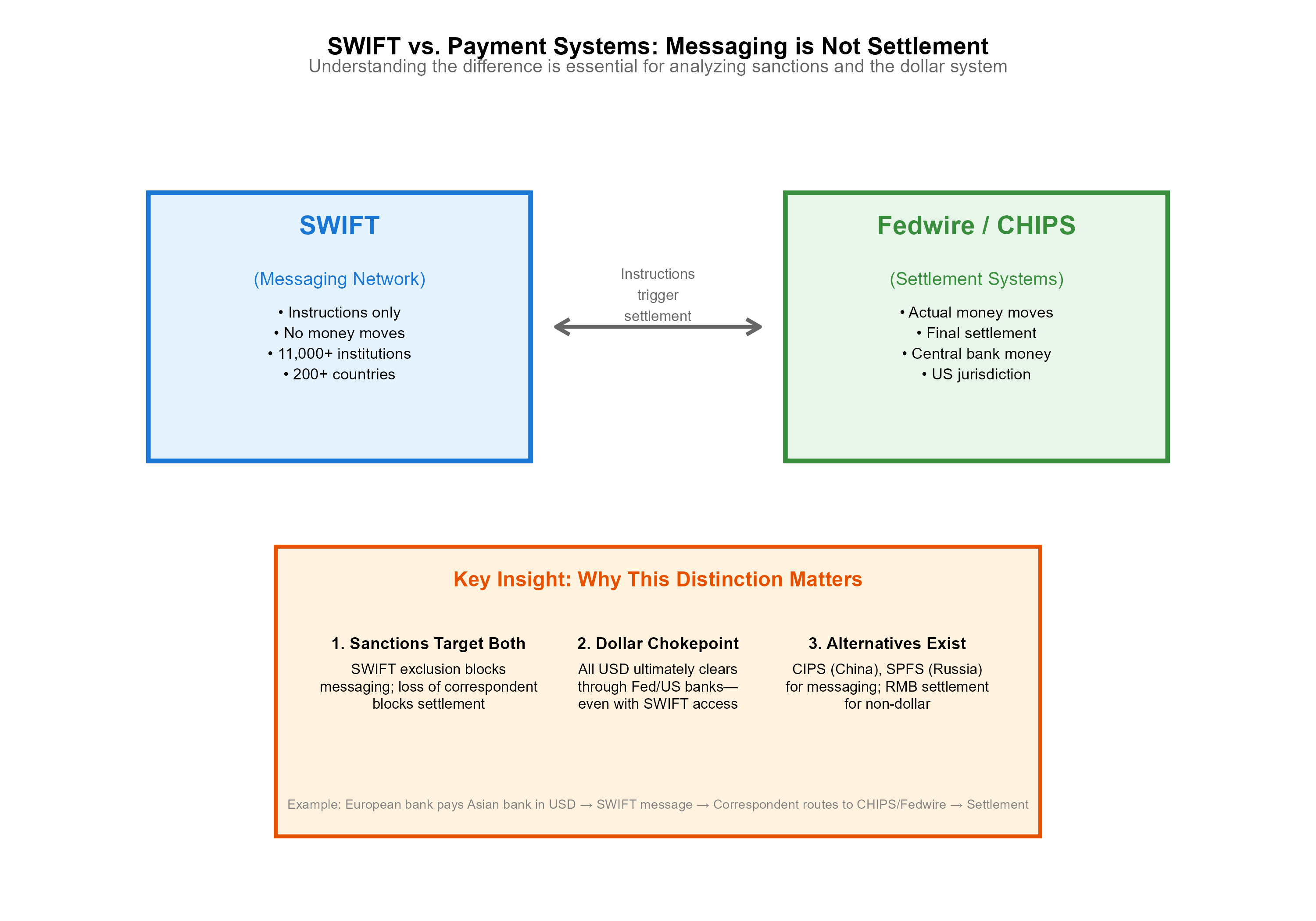

Figure 5.2: SWIFT vs. Payment Systems: Messaging is Not Settlement. SWIFT provides messaging; settlement occurs in separate systems like Fedwire and CHIPS. Illustrative.

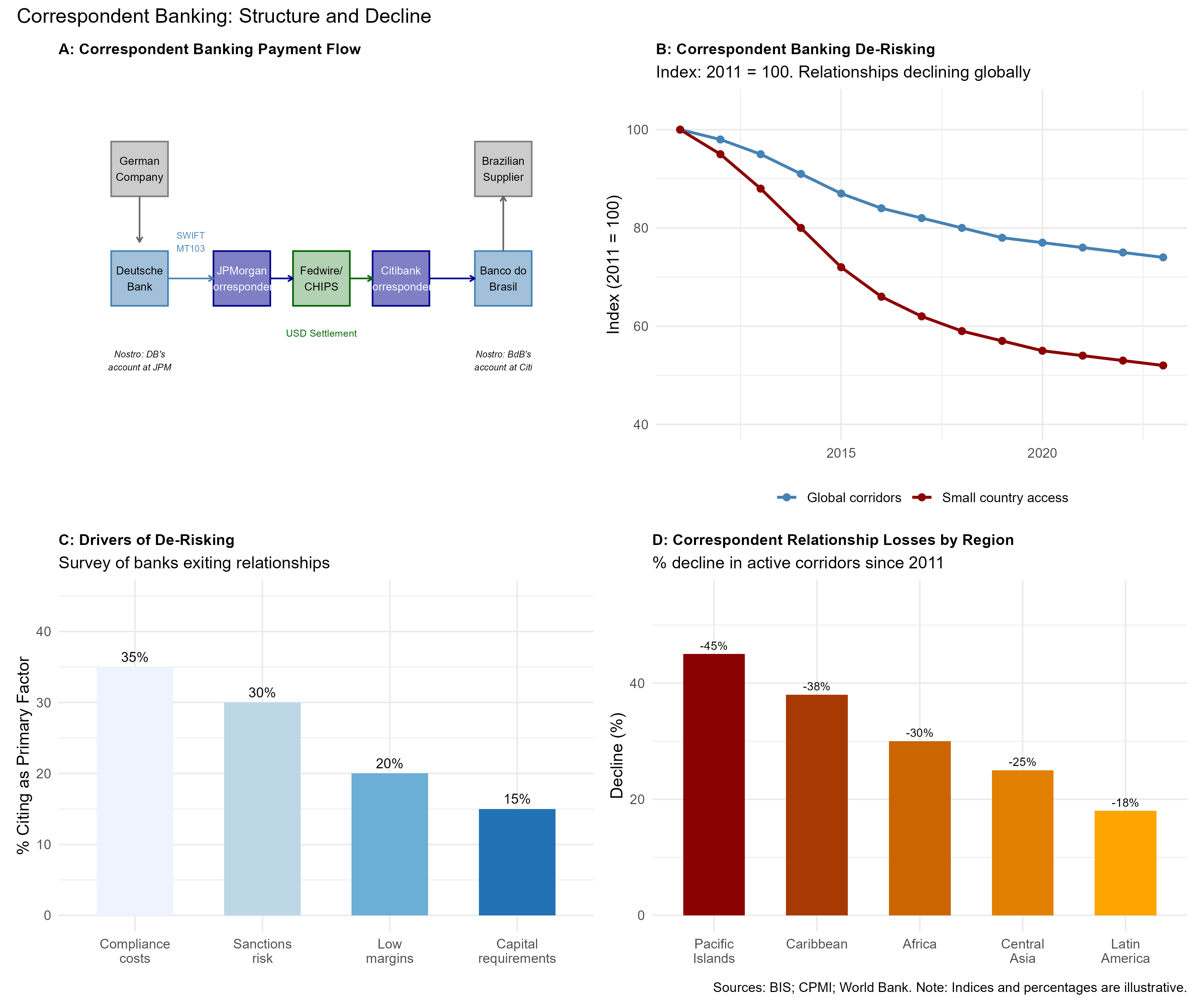

Figure 5.3: Correspondent Banking Networks. International payments flow through chains of correspondent relationships, with US banks as key nodes for dollar transactions. Illustrative.

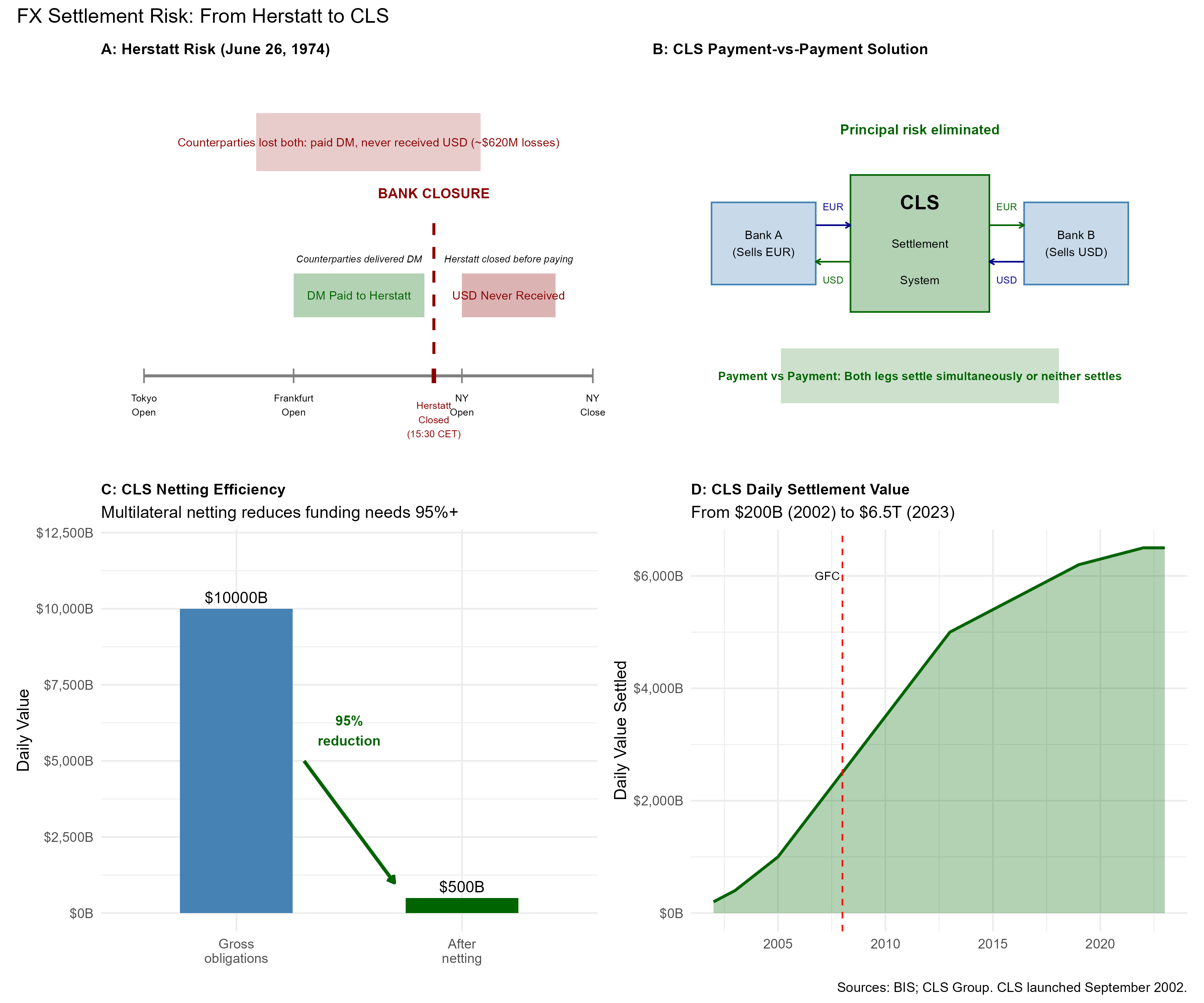

Figure 5.4: CLS and the Herstatt Problem. CLS eliminates FX settlement risk through payment-versus-payment, addressing the vulnerability revealed by Herstatt's failure in 1974. Illustrative.

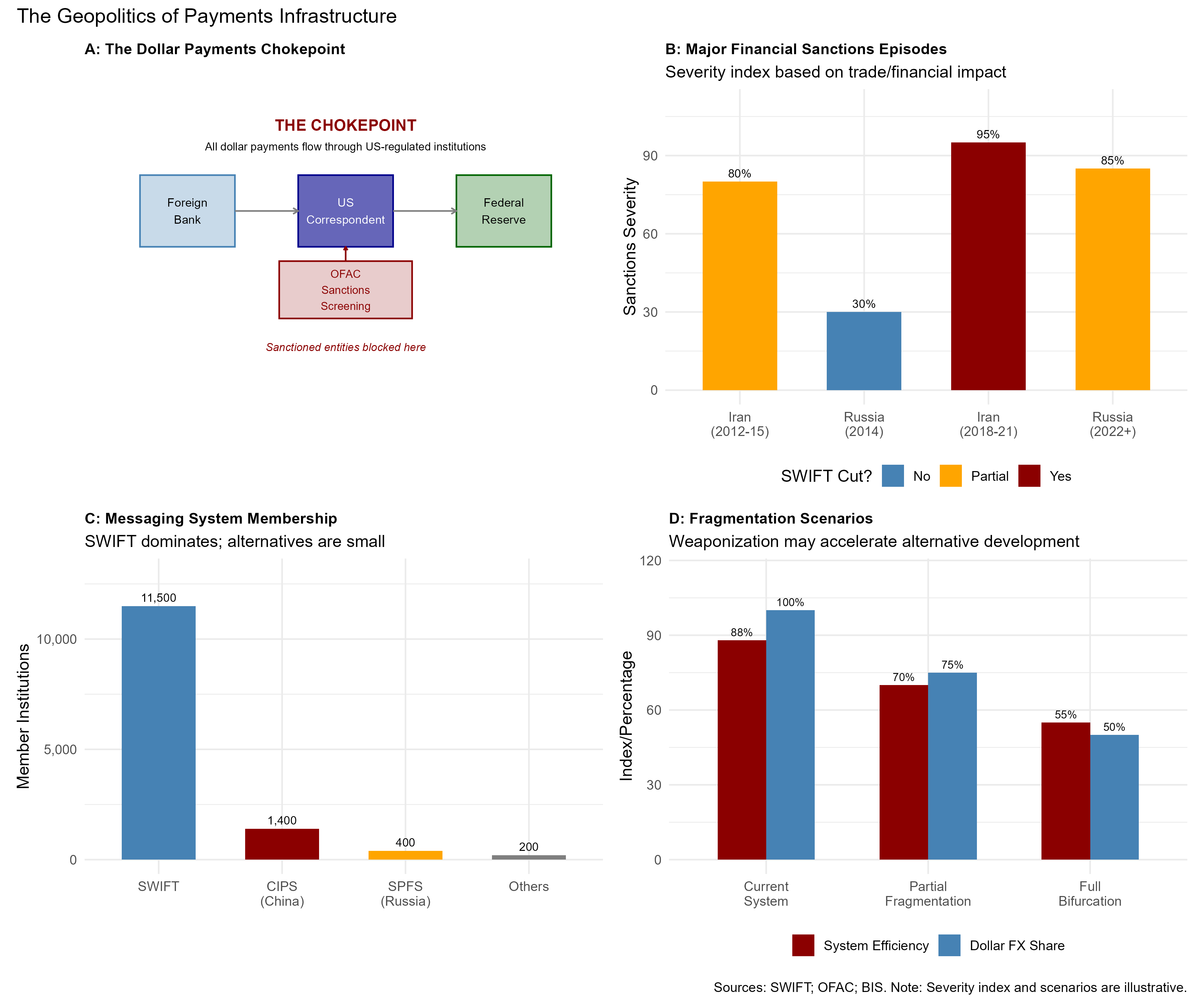

Figure 5.5: Payment Geopolitics and Alternative Systems. Countries are developing alternatives to dollar-centric infrastructure to reduce vulnerability to sanctions and exclusion. Illustrative.