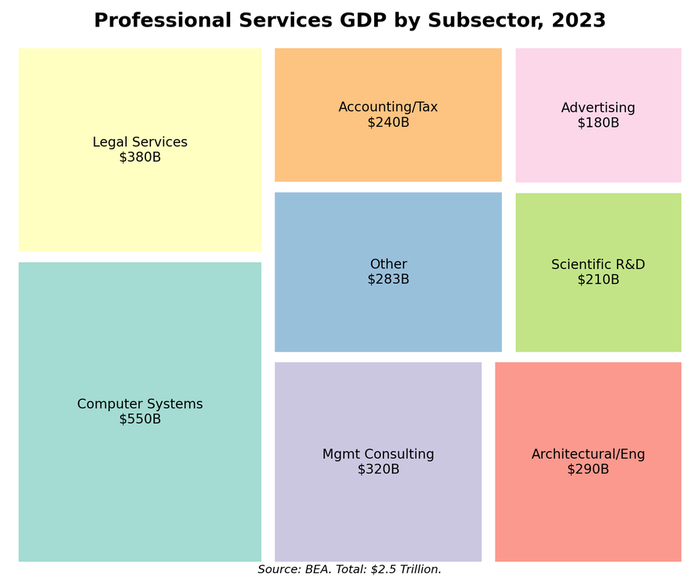

Figure 7.1: Professional services GDP by subsector. Computer systems design ($550B) has overtaken legal services and consulting to become the largest subsector, reflecting the economy's growing dependence on IT outsourcing and digital transformation. Source: BEA (2023)