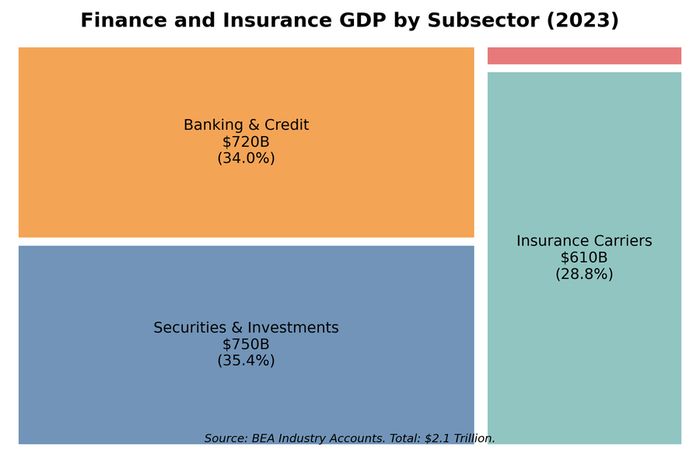

Figure 8.1: Finance and insurance GDP by subsector. Banking generates roughly half the sector's value-added, reflecting its central role in maturity transformation---borrowing short from depositors and lending long to homebuyers and businesses. Source: BEA (2023)