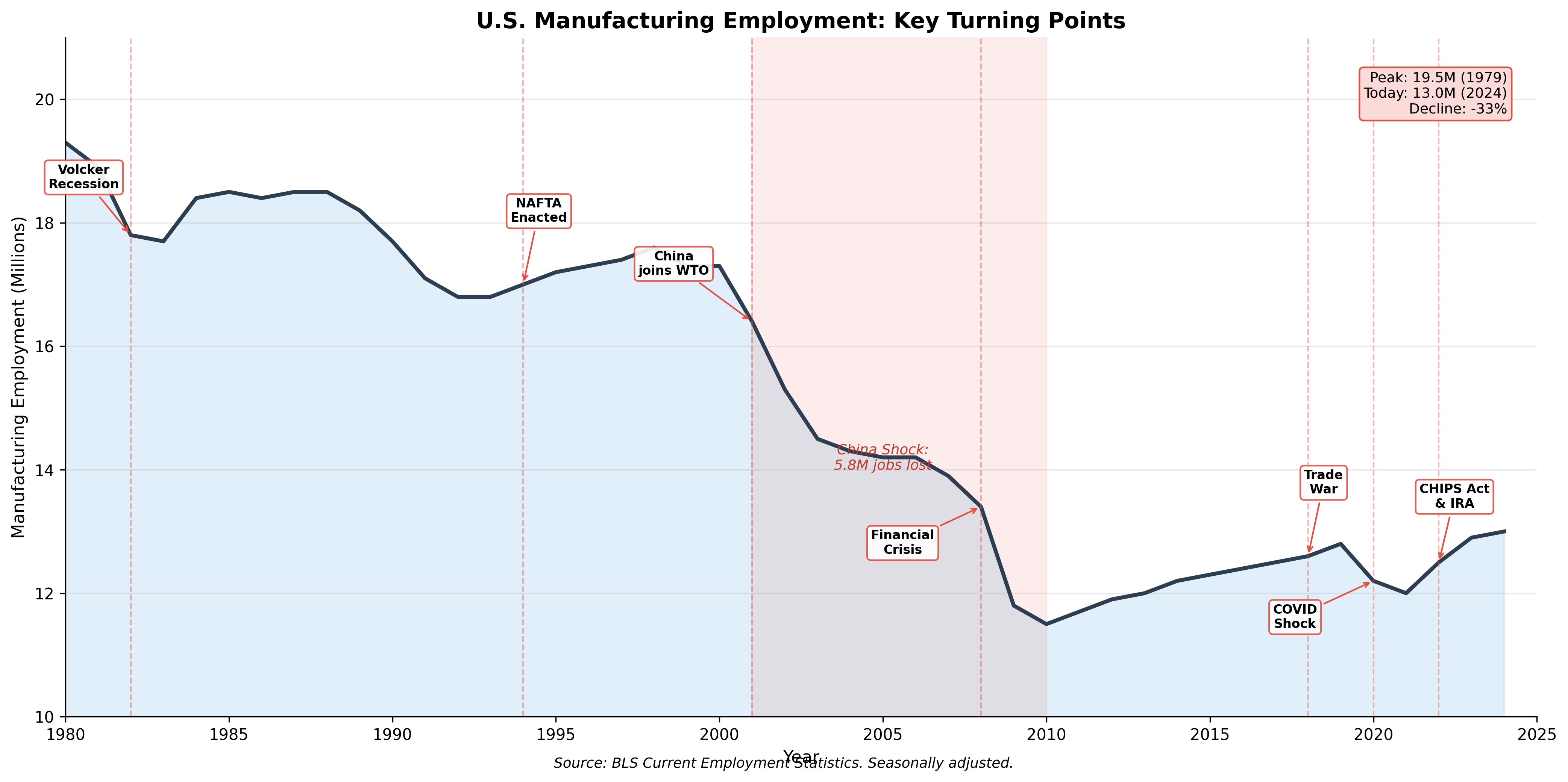

Figure 9.1: Manufacturing employment with key turning points, 1980-2024. Key events—NAFTA, China's WTO accession, the financial crisis, and the CHIPS Act—mark turning points in the sector's long employment decline. Source: BLS CES

Figure 9.1: Manufacturing employment with key turning points, 1980-2024. Key events—NAFTA, China's WTO accession, the financial crisis, and the CHIPS Act—mark turning points in the sector's long employment decline. Source: BLS CES

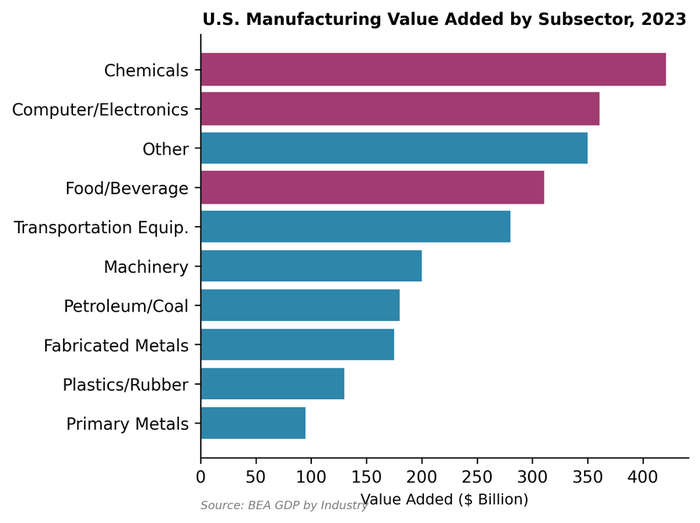

Figure 9.2: Manufacturing value added by subsector. Chemicals (including pharmaceuticals) and computers/electronics lead---high-value, capital-intensive industries that have survived offshoring, unlike labor-intensive sectors such as textiles and furniture. Source: BEA (2023)

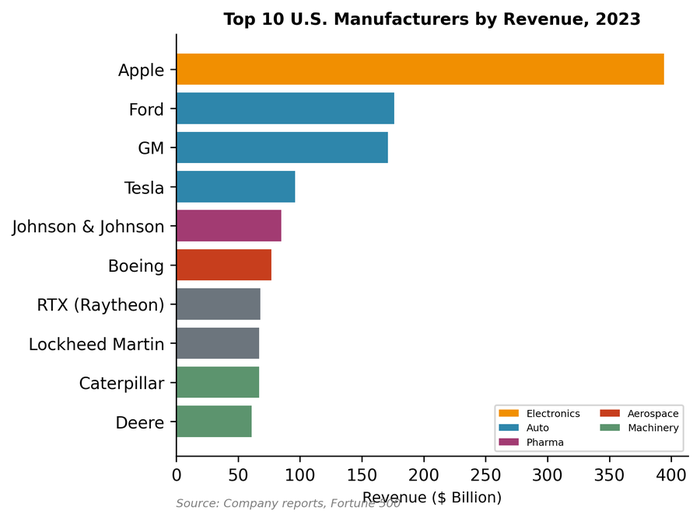

Figure 9.3: Top U.S. manufacturers by revenue. Apple leads by a wide margin despite owning no factories---it captures the lion's share of value through design and software while contracting all physical production to suppliers in China, illustrating how "manufacturing" increasingly means value capture, not production. Source: Company data (2023)

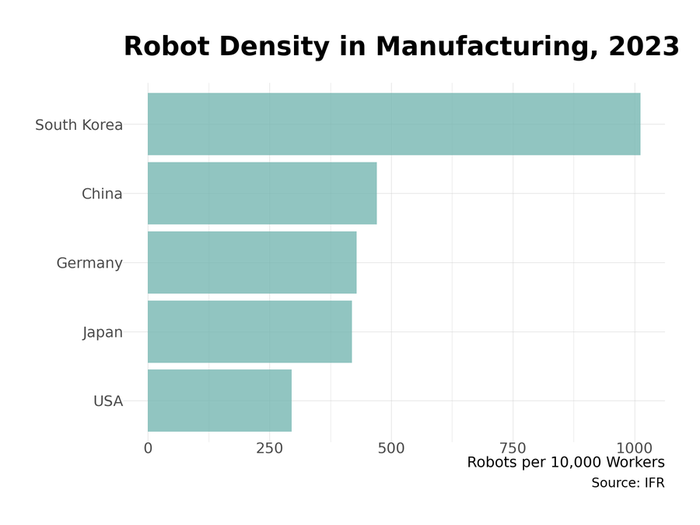

Figure 9.4: Industrial robot density (robots per 10,000 manufacturing workers). Despite its technological prowess, the U.S. (295 robots per 10,000 workers) lags South Korea (1,000) and Germany, and has been surpassed by China (470)---a gap that suggests continued manufacturing employment pressure as automation expands. Source: IFR (2023)

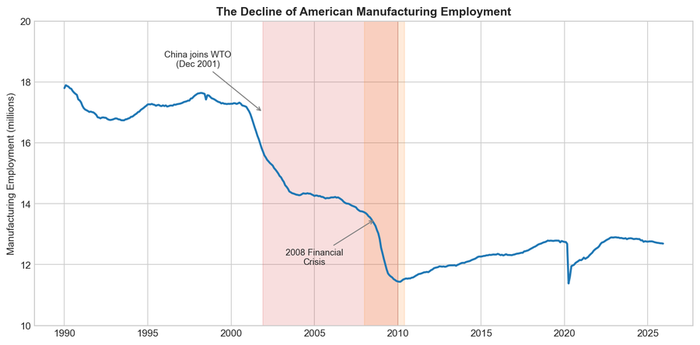

Figure 9.5: Manufacturing employment fell sharply from 17.3 million in 2000 to 11.5 million in 2010—a loss of 5.8 million jobs in a single decade. The China shock contributed substantially to this decline. Source: BLS