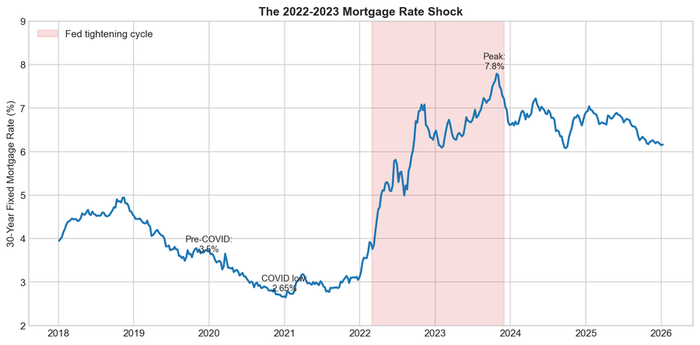

Figure 18.2: The 30-year fixed mortgage rate doubled from 3% to over 7% in just 18 months, the most rapid increase since the Volcker disinflation of 1981-82. Source: FRED

Figure 18.2: The 30-year fixed mortgage rate doubled from 3% to over 7% in just 18 months, the most rapid increase since the Volcker disinflation of 1981-82. Source: FRED

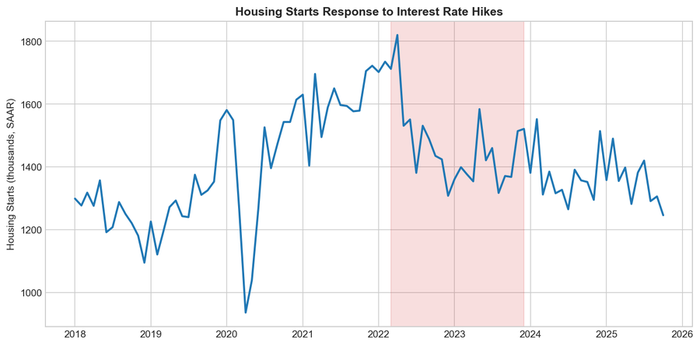

Figure 18.3: Housing starts fell sharply as mortgage rates rose, demonstrating the Fed's primary transmission mechanism to the real economy. Source: Census Bureau