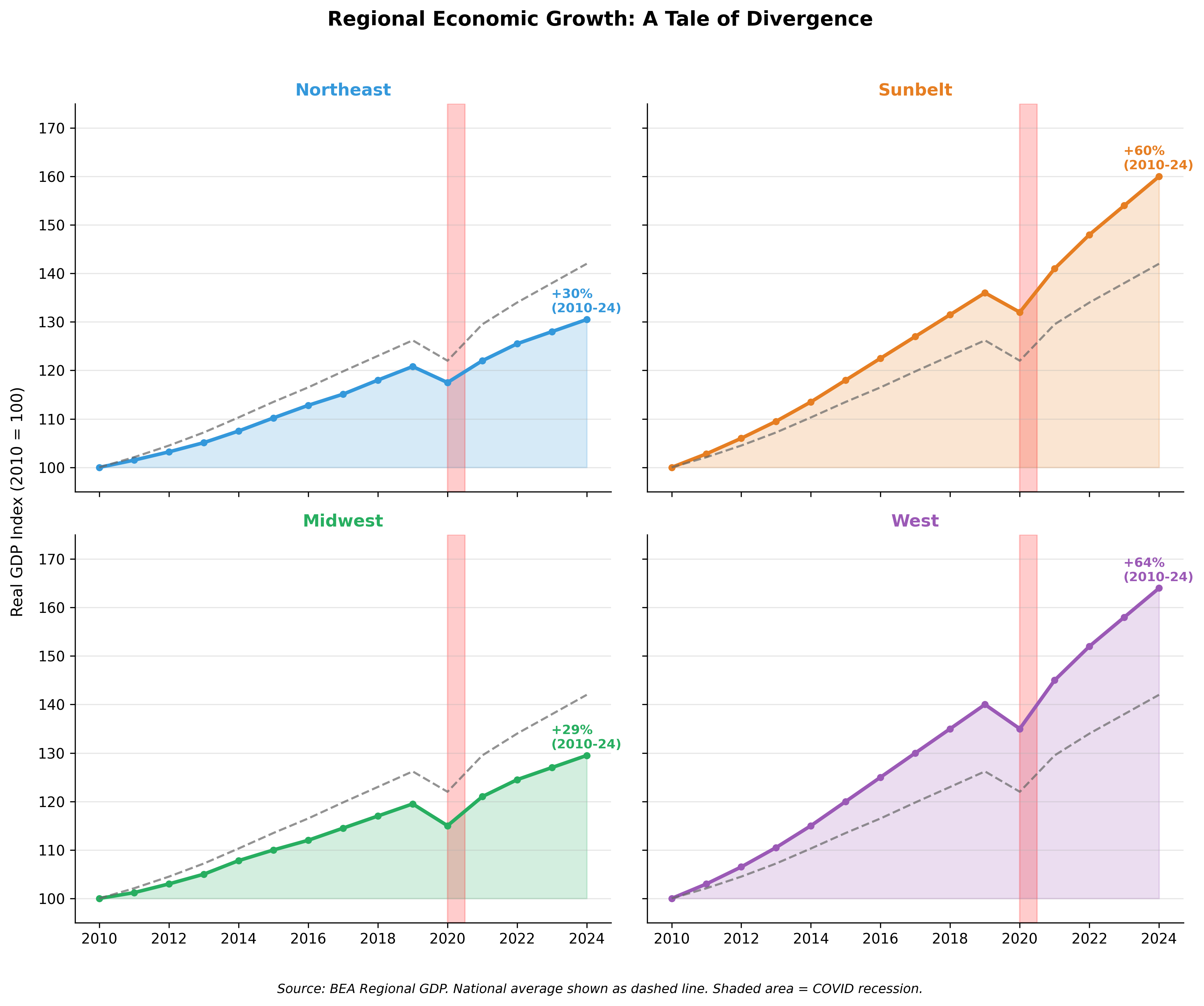

Figure 23.2: Regional economic growth trajectories (indexed to 2010). The Sunbelt and West have grown faster than the Northeast and Midwest over the past decade, though the COVID recession hit all regions. The dashed line shows the national average. Source: BEA Regional GDP