Figure 1.1: Real GDP Level and Growth Rate. Source: South African Reserve Bank, Stats SA.

Figure 1.1: Real GDP Level and Growth Rate. Source: South African Reserve Bank, Stats SA.

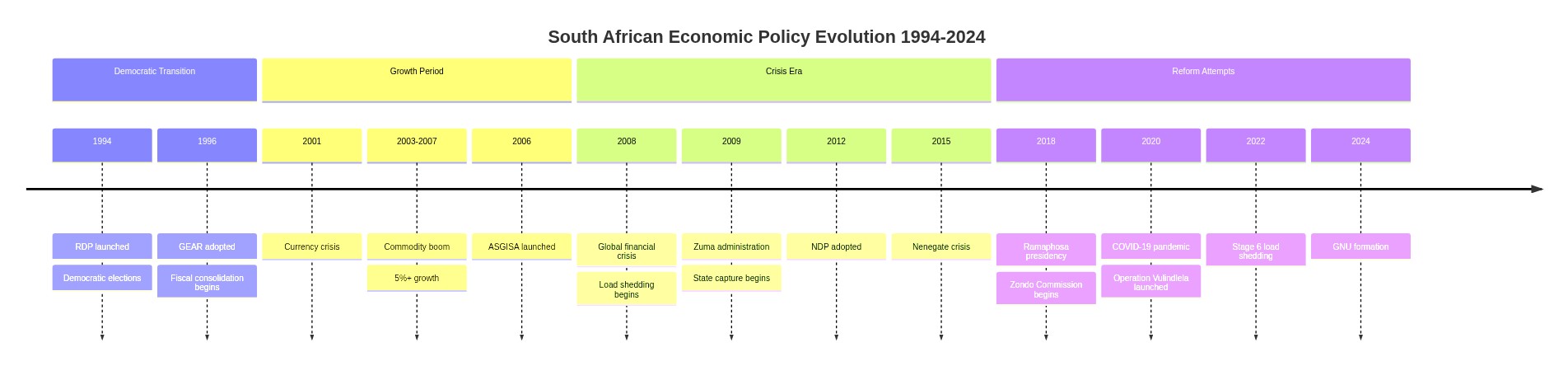

Policy timeline showing the evolution from RDP through GEAR, the crisis era, and reform attempts.

Figure 1.2: Gross Fixed Capital Formation (% of GDP). Source: World Bank, SARB.

Figure 1.8: The Investment Collapse: Public vs Private GFCF (% of GDP), 2000–2024. Source: SARB Quarterly Bulletin; National Treasury Budget Review. Public investment peaked with World Cup infrastructure and collapsed as SOE bailouts consumed fiscal space. Private investment never recovered from the GFC.

Figure 1.3: Government Debt-to-GDP Ratio. Source: IMF, National Treasury. Note: Debt tripled from 24% of GDP in 2008 to nearly 79% by 2025/26, where the 2026 Budget projects it to peak before declining.

Figure 1.4: Emerging Market Growth Comparison. Source: World Bank.

Figure 1.5: Policy Timeline (1994-2024). Source: Various government and academic sources.